Term Structure Of Interest Rates And Swap Valuation

Term Structure Of Interest Rates And Swap Valuation Option Finance Futures Contract

Solved Question 1 6 1 Point Term Structure Of Interest Ra Chegg Com

Finance Question Term Structure Of Interest Rates And Swap Valuation The Student Room

How To Value Interest Rate Swaps

Pdf Bond Pricing And The Term Structure Of Interest Rates A Discrete Time Approximation

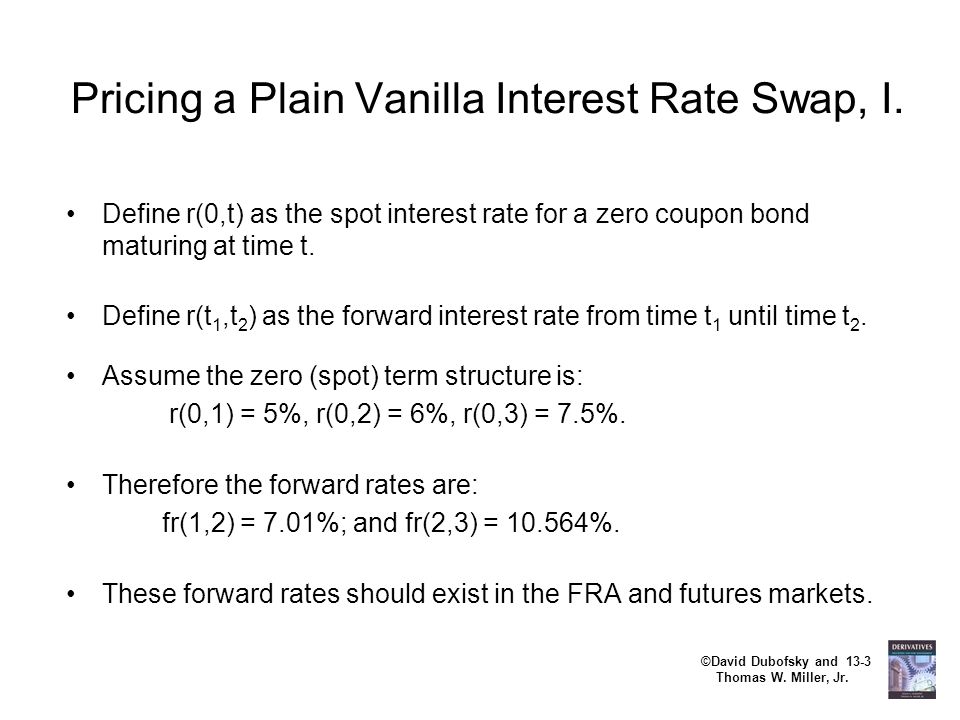

Chapter 13 Pricing And Valuing Swaps Ppt Download

Guide to simple dcf valuation excel ama leveraged finance analyst at a bb.

Term structure of interest rates and swap valuation. S1 s2 s3 s4 s5 s6 7 0 7 3 7 7 8 1 8 4 8 8 what is the discount rate. Term structure of interest rates and swap valuation suppose the current term structure of interest rates assuming annual compounding is as follows. S1 s2 s3 s4 s5 s6 7 0 7 3 7 7 8 1 8 4 8 8. Term structure of interest rates and swap valuation.

S1 s2 s3 s4 s5 s6 7 0 7 3 7 7 8 1 8 4 8 8 what is the discount rate d 0 4. S1 s2 s3 s4 s5 s6 7 0 7 3 7 7 8 1 8 4 8 8 what is t. Term structure of interest rates and swap valuation suppose the current term structure of interest rates assuming annual compounding is as follows. Suppose the current term structure of interest rates assuming annual compounding is as follows.

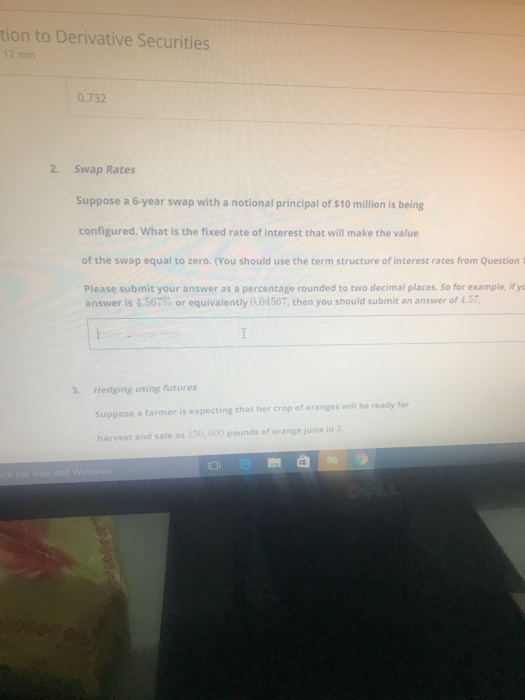

What is the fixed rate of interest that will make the valueof the swap equal to zero. Suppose the current term structure of interest rates assuming annual compounding. S1 s2 s3 s4 s5 s6 7 0 7 3 7 7 8 1 8 4 8 8. Swap ratessuppose a 6 year swap with a notional principal of 10 million is beingconfigured.

Term structure of interest rates and swap valuation suppose the current term structure of interest rates assuming annual compounding is as follows. Term structure of interest rates and swap valuation suppose the current term structure of interest rates assuming annual compounding is as follows. Term structure of interest rates and swap valuation. What is the discount rate eq d 0 4.

Interest rates are both a barometer of the economy and an instrument for its control. You should use the term structure of interest rates.

Pdf Interest Rate Risk Management Developments In Interest Rate Term Structure Modeling For Risk Management And Valuation Of Interest Rate Dependent Cash Flows

Chapter7 Swaps Ppt Download

Pdf A Theory Of The Term Structure Of Interest Rates

Term Structure Of Interest Rates Definition

Swaps Types And Valuation Ppt Download

Asset Swap Wikipedia

Ois Swap Pricing Valuation Ois Vs Libor Financetrainingcourse Com

Pdf Dynamic Interactions Between Interest Rate And Credit Risk Theory And Evidence On The Credit Default Swap Term Structure

Pdf Pricing Stock Options With Stochastic Interest Rate

Amortizing Accreting Swap Pricing And Valuation Finpricing

Pdf Understanding Cva Dva And Fva Examples Of Interest Rate Swap Valuation

Https Arxiv Org Pdf 1803 02249

Http Finance Wharton Upenn Edu Nroussan Syllabus Spring2014 Pdf